Long and thus far wrong on TIGO

I started a position in TIGO earlier this year as the stock collapsed after a botched rights offering that led to 70%!! equity dilution and took the stock down from $25 down to $17. I have purchased it all the way down averaging $14.03 thus far. It is a top 10 position for me which is basically saying something since I have basically ~10 positions. I won’t go too deeply into TIGO’s business other than to say it is a wireless telco operator in 9 countries in Latin America in addtion to offering broadband through cable and some Fiber assets in a parts of its Latin American footprint. For those interested in more detailed descriptions of the business there are a couple of excellent write ups on it available on the web.

https://www.valueinvestorsclub.com/idea/MILLICOM_INTL_CELLULAR_SA/7871947735

Those links offer a wealth of information on TIGO in terms of describing the business. A short pitch is basically buying a leading wireless and broadband company in emerging markets where penetration of 4G and broadband is still below 50%. ARPU is very low and has plenty of room to grow as well. The company is either number 1 or 2 in 8 of its 9 markets in wireless. Its broadband footprint is much more limited and the company has been spending to expand its footprint. As such cap ex is relatively elevated. It has strong margins and competition in its two most important markets, Guatemala and Panama is limited. It has grown quickly in Colombia but faces a more competitive environment there and it has wisely chosen partners to grow in that market.

That is a easy visual description of what we are buying in TIGO.

So why do I own this? Well it basically boils down to is this a good business with a moat around it and second it is priced at a reasonable valuation? And also is it run by a strong management team with a proven track record?

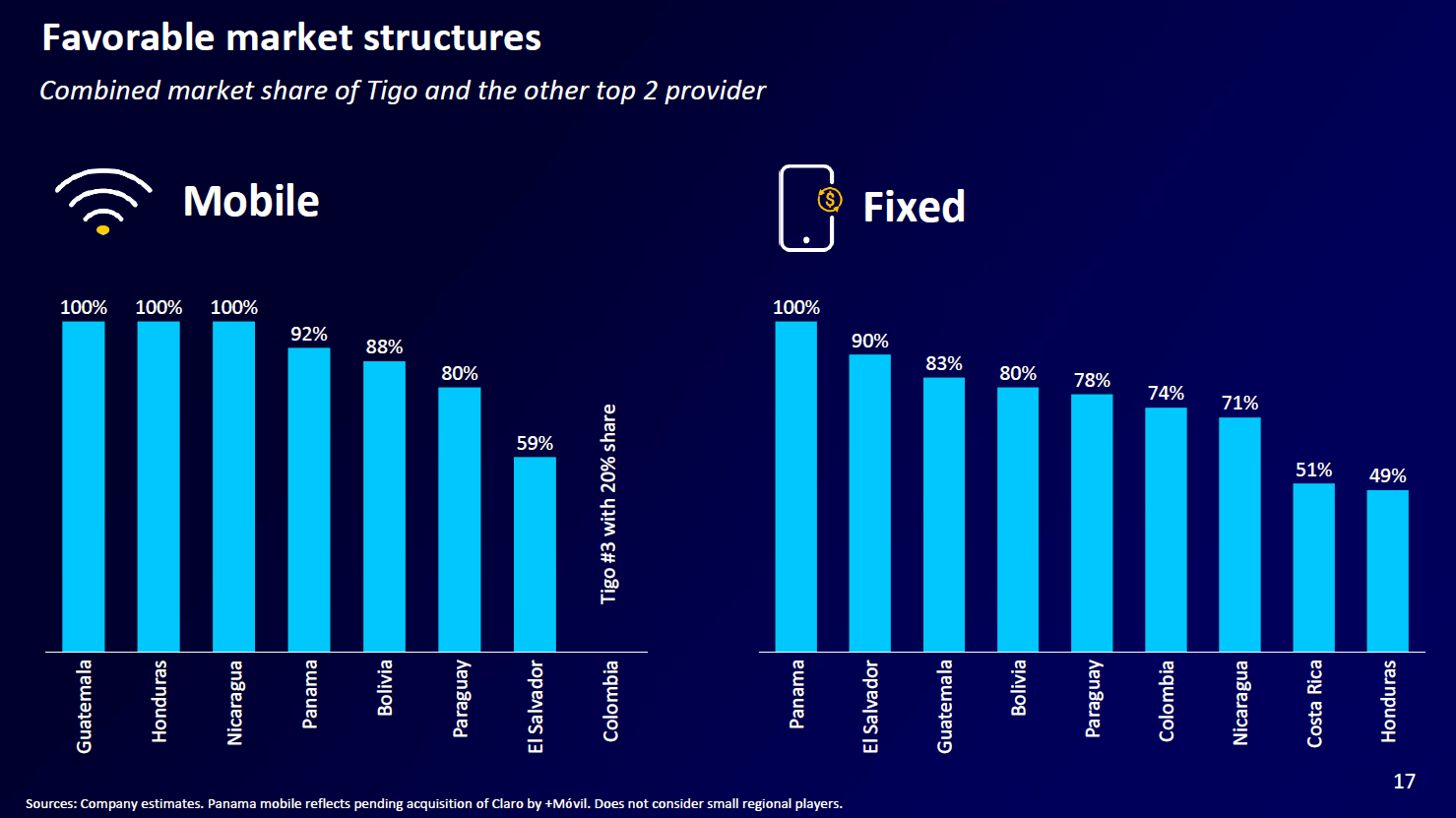

The answer to the first question is basically one of how easy it for new competition to upset the duopoly market structures in most of its wireless markets to create an environment similar to what scrappy number 3 T-Mobile did to VZ and AT&T in the US? I believe the answer here for at least the foreseeable future is no. As such TIGO will continue to enjoy strong margins in its core markets and will use cash flow to continue to build out its 4G and 5G infrastructure and continue to invest in its broadband footprint. The recent uptick in cost of debt capital has made new entrants even more unlikely. Given the increased cost of capital it likely will also lead to TIGO slowing down its own expansion plans. The company has guided for annual cap ex of $1B going forward and cumulative 3 year ‘22-25 fully levered FCF of $800M-$1B.

Its management team is a bit of conundrum. The CEO Mauricio Ramos was the former President of Liberty Latin America and is a John Malone disciple. At one time that was quite prestigious but the market has recently soured on the “cable cowboy”. IMHO the management has done a good job growing and operating the business. However, after the completely botched and poorly times rights offering their capital markets grade is a D at best. I have wrestled with this as apotentially disqualifying factor for a potential investment here but I decided to give them a pass this time because the rest of their debt structure is relatively clean and their avg cost of debt is 5.8% with 40% of debt in local currencies, reducing FX risk.

VALUATION

TIGO has ~170M shares outstanding a equity cap at $12 of $2.04B.

It has net debt of $6B and operating leases of $1B.

So the EV including leases if ~$9B.

2022 1H EBITDA has been $1.15B and full year EBITDA should be just north of $2.3B

2023 EBITDA estimates are ~ $2.45B.

On 2023 EBITDA numbers the business is trading at ~3.7x EV/EBITDA.

Pre COVID the business traded at 7-8x EBITDA but that was during the period where the risk free was much lower so at this point that multiple is not realistic. Meanwhile US operators such as VZ and T have de rated to 7x EBITDA while TMUS still trades at 9.5x EBITDA. Meanwhile in the cable space CMCSA and CHTR have seen their valuations collapse to 6-7X EBITDA as both are no longer growing meaningfully. The US competitive landscape is considerably tougher than TIGO’s.

So with US players trading at say 6-7X what discount does TIGO deserve? Given emerging market risks it certainly deserves a discount. However, its growth potential is vastly superior to the mature and highly competitive US market. On a fully levered basis if we assume ~$300M in FCF we have an equity FCF yield of ~14-15%. On an absolute basis for a business which outside a big global recession has growth ahead of it, I believe this is quite cheap.

The company has a Fin Tech unit called TIGO Money which thus far has consumed capital but has grown nicely. For simplicity I am valuing this at Zero for now although I do believe it has significant value and potential.

Lastly, the company owns all its wireless towers and a few data centers as well. It has been working on a plan to split its Towers business and sell a 50% stake in the business to a Infrastructure players. The towers would be leased back for 10 years and the TowerCo would likely get at least 10x EBITDA which at the recent GS conference the CEO suggested would be ~$100M. Selling a 50% stake at 10x would net the company $500M. In addition the FCF effect would be neutral according to CEO as they would save on cap ex which would offset the EBITDA hit. This sounds dubious but the $500M in cash they can raise is real so I will dock them for $20M in FCF next which is not material at their current valuation. This transaction looked a lot better 6 months ago but would still deleverage the balance sheet to below 3x which is mgtm goal.

I am definitely mindful of the recent currency upheaval form the USD jump but thus far that has been a non event for Latin American currencies which have been relatively stable and TIGO’s debt is largely fixed and only 60% if denominated in US$. NOt sure what added multiple discount this warrants.

So I am long and wrong…but at a 15% FCF yield I am holding strong…

I will post this on Twitter and I would love to hear thoughts and criticisms.

Thanks for reading.